Engineer News Network The ultimate online news and information resource for today’s engineer

Engineer News Network The ultimate online news and information resource for today’s engineer

The escalation of conflict in the Middle East is placing global fertiliser supply chains under growing strain, disrupting production, exports and trade flows across nitrogen, phosphate and sulphur markets. With the Strait of Hormuz handling roughly a third of global fertiliser trade, the near-closure of the route and attacks on regional energy infrastructure have created logistical bottlenecks, higher freight and insurance costs, and rising uncertainty among producers and traders. Market activity has slowed as participants wait for greater clarity, with some producers expected to hold back offers for up to 10 days while assessing the evolving situation. Chris Vlachopoulos reports

The global fertiliser market has entered a new phase of volatility as the escalation of the conflict across the Middle East reverberates through nitrogen, phosphate and sulphur fertilizer products.

The sudden disruption to production and exports from key producers in the Arab Gulf, compounded by the near-closure of the Strait of Hormuz, has triggered uncertainty just as several regions prepare for fertiliser application season.

Market participants cite rising freight, insurance and operational risks, with logistical constraints now a key concern.

A trader said: “Let’s wait”. Referring to phosphates demand in India, he said: “[I] believe no one [will] offer this week, as the producers may want to wait more.”

Asked on any business updates, they added that they expect nobody to offer any product over the next 10 days, describing the situation as ‘scary’.

While fundamental demand from farmers remains largely subdued, the supply shock has jolted pricing across nitrogen and urea.

The interruption of the flow of ammonia, urea and sulphur from the Middle East, a key supplier for all products, has further tightened markets already strained by earlier gas disruptions, winter curtailments, and ongoing geopolitical issues affecting Russia and China.

As producers, traders and buyers navigate a fast-moving situation, risks are building and participants are bracing for several weeks of disruption.

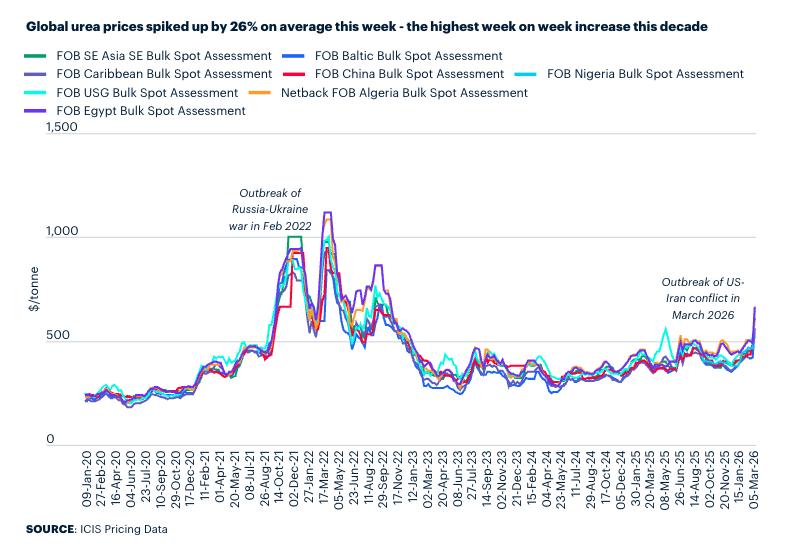

Urea

Urea prices have surged as much as 35% to three-year highs as buyers are scrambling for alternative supply after the US-Iran war disrupted shipments and production in the Middle East.

Traders covered short positions in North Africa and southeast Asia, while some have even started building long positions as they expect the conflict involving the US, Israel and Iran to last for at least another month.

Actual end-user demand remains minimal, with farmer incomes still under pressure as crop prices post only modest gains and are nowhere near the surge seen in fertiliser.

The timing of the conflict is particularly bad for global agriculture, as many regions that depend heavily on Arabian Gulf urea supplies are about to begin their fertiliser and urea application season.

Farmers in the US are preparing to apply fertilizer for spring, while India has confirmed just over 500,000 tonnes from the Arab Gulf for shipment by 31 March to stock up ahead of kharif, or monsoon, application.

Any available cargoes in Brazil are being diverted to the US where prices are higher. Indian output is beginning to be cut due to gas issues, while a plant also shut down in Pakistan.

Buyers in Australia and southeast Asia will need to seek alternative suppliers, while European farmers, about to begin their application season, face a double blow from rising global prices and the added cost of the EU’s Carbon Border Adjustment Mechanism (CBAM).

Attacks on energy infrastructure are worsening the disruption, with QatarEnergy stopping production of urea and ammonia after halting output of liquefied natural gas (LNG) on 2 March, and then declaring a force majeure.

The Strait of Hormuz handles a third of global fertilizer trade, with exports from the Arab Gulf expected to be unavailable for at least four weeks.

Monthly exports from the Arab Gulf are estimated at over 1.5 million tonnes of urea, while Iran accounts for another 350,000-400,000 tonnes/month.

War-related damage to plants and infrastructure is expected to prolong the disruption even further even if the Strait of Hormuz opens soon.

Global urea supplies were already tight ahead of the Middle East conflict due to gas disruptions in Iran during the winter and as Chinese exports are absent, while Ukrainian drone strikes to Russian nitrogen plants have also hit supply.

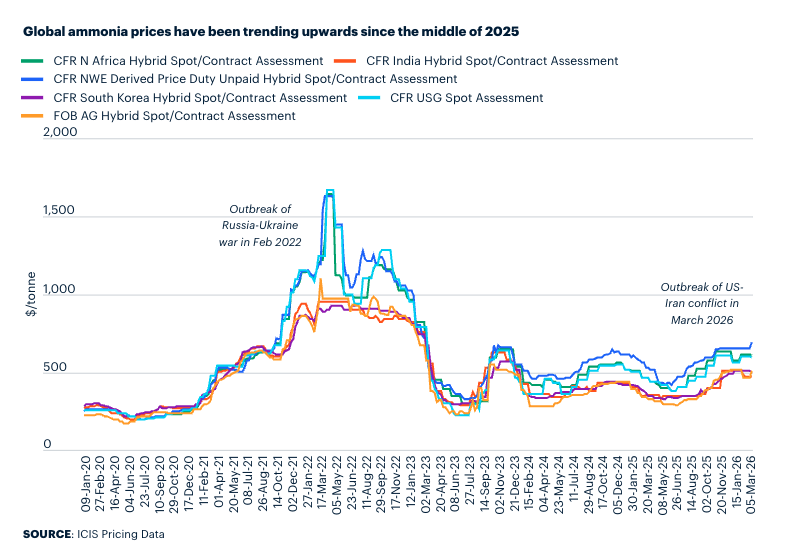

Ammonia

The escalation of the Iranian conflict has affected the ammonia market, as the region is a main exporter to the east and the west. Some buyers are already expecting their cargoes which are out of the Strait of Hormuz, but other vessels are stuck in the region.

This has led to increased buying interest for southeast Asianmaterial, with Indonesian and Malaysian producers offering tonnes and offer prices in the region edging upwards.

The lack of Iranian material is also expected to affect India due to suspension in gas supply from Qatar.

Also, a lack of ammonia imports from the Middle East is expected to affect the phosphates market, with Indian phosphates producers needing ammonia soon after they finish their scheduled maintenance.

Following the events in the Middle East, natural gas TTF prices rose during the week forcing some European producers to withdraw offers. An Algerian cargo sold to Europe at higher levels signalled the trend that the market is facing.

Moreover, in another move that will affect farmers, the European Commission insisted that fertilizers will remain covered by the Carbon Border Adjustment Mechanism (CBAM).

In the Americas, the Tampa March contract price was settled at a decrease, despite participants expecting higher prices on tight availability. The Gulf Coast Ammonia plant is still down until mid-March and Nutrien’s operations in Trinidad remain shut on natural gas supply issues.

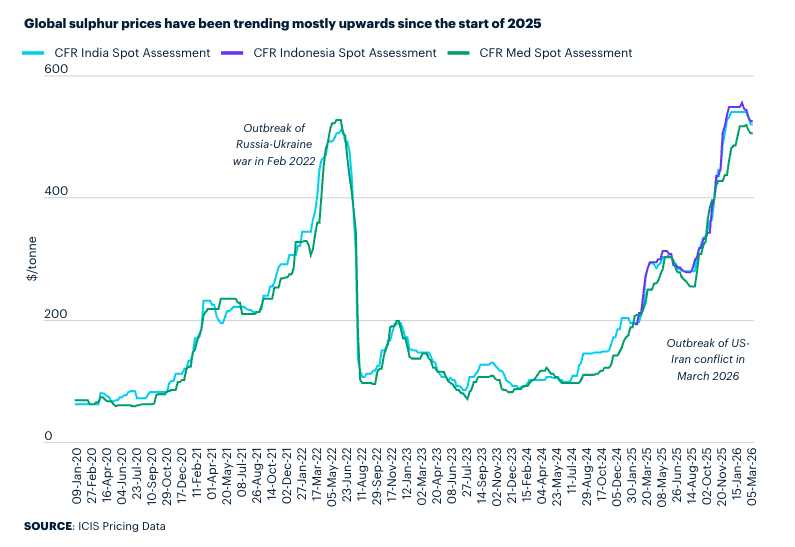

Sulphur

Global sulphur trade has stalled as producers, traders and buyers await clarity on the wide-ranging impacts of a new conflict in the Middle East – and any guidance on how long the fight will continue.

On 28 February, the US and Israel launched a surprise wave of missile attacks on Iran, which retaliated against neighboring countries in the Arab Gulf, raising concerns about a much wider conflict and threatening global oil and chemicals supply.

Immediate effects have been seen in higher freight costs, insurance, and logistical snags affecting sulphur and many other downstream fertiliser and chemicals products – the greatest of which is the near-closure of the Strait of Hormuz.

News of the airstrikes came just days after global sulphur costs had finally started to decline after months at record highs.

Offer prices in Indonesia, the Mediterranean and India were all slipping late last week as buyers stepped back from purchasing amid expectations of further declines.

At the time, there was some debate if these declines represented a correction from previously inflated levels, or were simply the result of China – the world’s largest sulphur importer – only just returning from Lunar New Year holidays. This is likely a moot point now, however, after the US-Israel attacks on Iran.

Although this week’s sulphur pricing is largely stable in the absence of trading, the mood is bullish – and this will intensify the longer the war continues.

Sulphuric acid

Just one week after burner feedstock sulphur pricing finally started to slide from record highs, a new conflict erupting across the Middle East made any chance of a continued decline appear near-impossible.

Although few nations in the region import large volumes of sulphuric acid – excepting Saudi Arabia – the knock-on impact of the conflict will eventually be felt across freight rates, insurance costs and bunkers, plus oil, gas, energy and food costs all the way back to consumers.

The availability of sulphuric acid-capable tankers will also likely be affected the longer the conflict continues, with many vessels at anchor either end of the Strait of Hormuz unable to transit without protection.

The conflict is yet to result in a large price swing for sulphuric acid, with sources discussing a mild uptick amid continued uncertainty and no rush on purchasing so far.

Purchase tenders in India and Argentina may offer some price direction as the world adapts to another shift in trade flows – and players ponder how long this new Middle Eastern unrest will last.

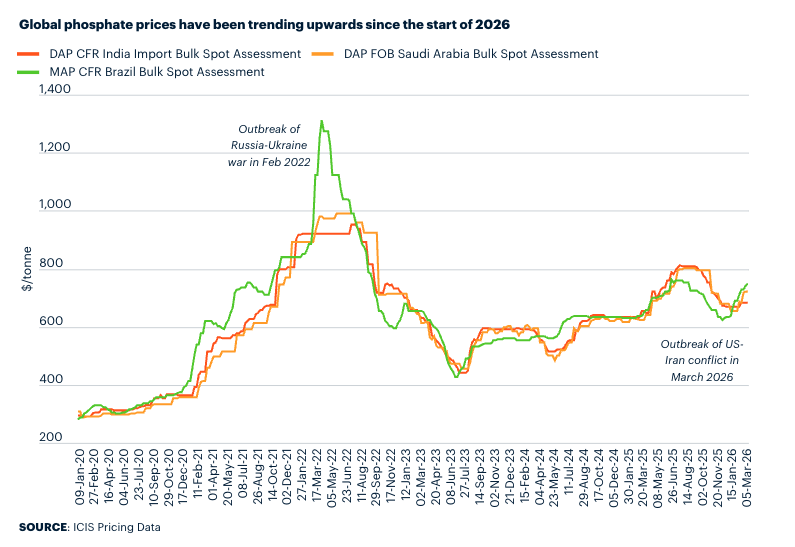

Phosphates

The phosphates market experienced a week of heightened uncertainty due to the Middle East conflict.

Price sentiment is firming across several regions amid geopolitical risks, logistical challenges, as well as a general pullback in spot activity and offers from producers.

In India, there were no fresh diammonium phosphate (DAP) activity or offers indicated. A local holiday, coupled with the fallout from the Middle East conflict, contributed to the slowdown.

Participants expect sellers to remain out of the market for at least 10 days, as producers assess risk exposure. Both buyers and sellers were described as highly cautious.

While seasonal demand is expected to pick up in the coming weeks, near-term trading is dominated by risk aversion. There were no updates on the RCF tender for various nitrogen phosphorus and potassium (NPK) products.

In Egypt, NCIC concluded its latest sales tender (closed 5 March) for March loading for DAP and triple superphosphate (TSP).

No new business was indicated in Saudi Arabia as producers face significant logistical constraints linked to the conflict, limiting their ability to place product in key markets.

This affects regions as far away as Australia, where participants indicated vessel delays for both the east and west coasts, with some vessels still waiting to enter the Gulf to load. Despite this, east coast supply is expected to remain adequate, but western Australia could face tighter supply situations.

Freight costs were a considerable concern for participants this week as well, contributing to the overall cautious sentiment.

Most of the activity this week centered around the US, particularly New Orleans (Nola). Expectations for lower summer-fill values faded, with a wave of fresh buying from participants. DAP barge values rose sharply, with multiple trades for March loading.

Brazil sentiment was dominated by the Middle East conflict, with importers and suppliers separately opting to step back from discussions.

The monoammonium phosphate (MAP) market remains tight, with few offers and major producers separately staying out of the market. Participants highlighted that Saudi Arabia is Brazil’s second-largest MAP supplier, raising concerns about supply given the regional conflict.

Potash

Demand for muriate of potash (MOP) is steady; with the fertiliser so-far avoiding the increased cost burden felt by competing nutrients stemming from the ongoing Middle East conflict.

Potential price hikes may lie ahead as producers pass increased insurance and freight costs to buyers, but as-yet shipments continue as planned.

In spot news, India’s NFL is in search of a maximum 60,000 tonnes for shipment by 30 April; while Brazilian import offers have ticked up slightly despite buyer

resistance.

Chris Vlachopoulos, Senior Editor for Phosphates at ICIS. ICIS delivers independent commodity pricing and analytics, news, market intelligence and insight across global chemical and energy markets.