Engineer News Network The ultimate online news and information resource for today’s engineer

Engineer News Network The ultimate online news and information resource for today’s engineer

William Beacham explains how pressures global chemicals industry are accelerating the move away from export-driven models. While major projects such as Borealis’ PDH unit and INEOS’ Project One cracker are still progressing, consolidation is expected as only the most competitive producers survive. The focus is shifting toward regional resilience, defence-linked demand and circular economy solutions as the industry adapts to a more protectionist global trading system

The global chemical industry is entering a period of profound uncertainty as higher tariffs and escalating trade tensions threaten to dismantle decades of globalisation.

Since US President Trump’s 2 April Liberation Day marked the start of the latest trade war, major economies have struggled with slow or stagnant economic growth, while chemical producers face low prices, margins and disrupted supply chains.

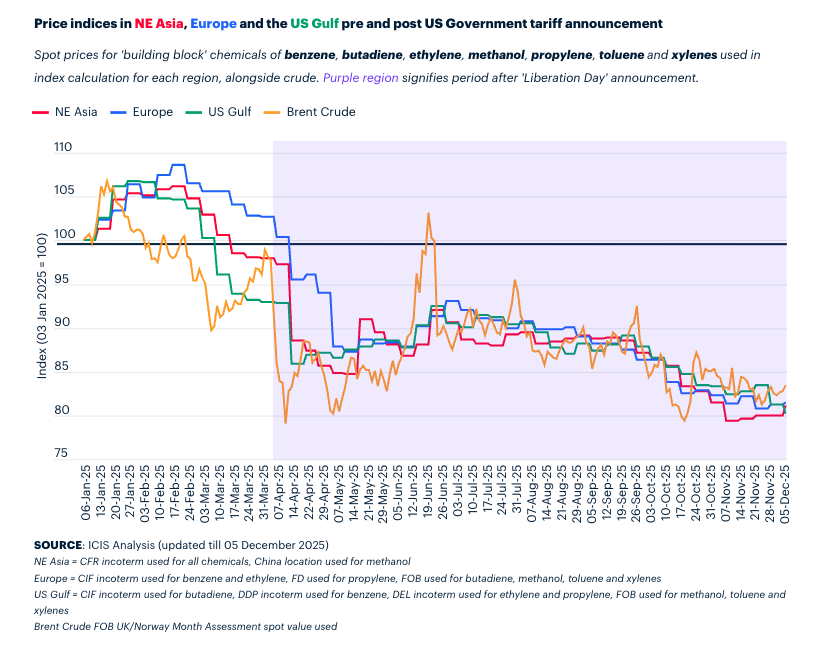

Average US tariffs surged from 2.4% at the start of the year to a peak of 28% in April before settling at 16.8% — the highest level since 1935. This sharp increase has weighed heavily on global trade flows, undermining confidence and delaying investment decisions. For chemical companies, the implications are stark: export-driven business models that dominated for decades are now under threat.

Rgeionalisation as a survival strategy

Across the industry, a shift toward more local or regional supply chains is gaining momentum as companies reassess business models to reduce exposure to geopolitical risk and tariff volatility.

European producers, already under pressure from weak demand, face additional challenges as the pending US-EU trade deal could eliminate tariffs on US finished goods and chemicals such as polyethylene (PE), which is currently subject to a 6.5% tariff.

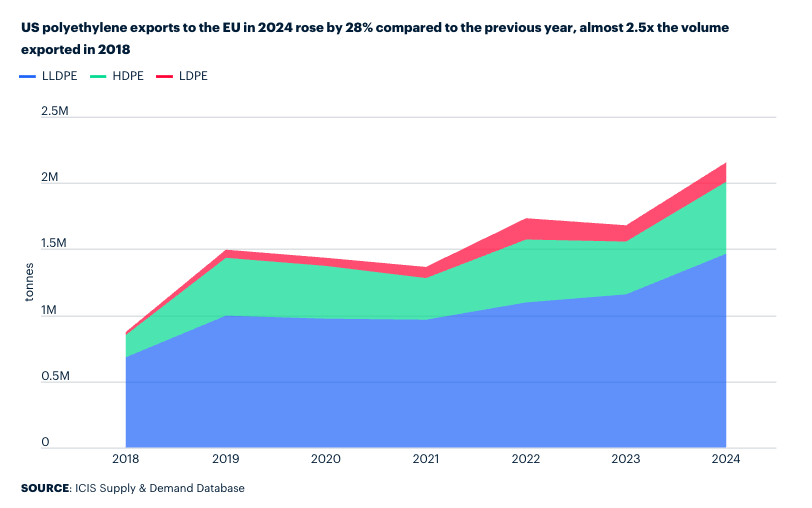

US PE exports to Europe have already rocketed as the country ramped up its ethane-based capacities.

At the same time, Chinese exporters may target Europe as an alternative market if US barriers persist, raising the risk of oversupply.

There are calls for more regulatory protection for European industrial value chains, including chemicals. There is a risk the region may become too reliant on imports rather than having a resilient domestic industrial backbone.

Chemicals projects under pressure

Despite these headwinds, some large-scale projects are moving forward. Borealis’ 750,000 tonnes/year Kallo, Belgium, propane dehydrogenation (PDH) unit is scheduled to start up in Q2 2026, while INEOS’ Project One cracker is expected online by early 2027.

Together, these ventures will add significant olefins capacity to a market already grappling with overcapacity. Meanwhile, Grupa Azoty’s $1.8 billion PDH-polypropylene project faces uncertainty after its special-purpose vehicle filed for bankruptcy protection.

The question is whether Europe can sustain these investments amid structural change. Consolidation appears inevitable, with a handful of efficient players likely to dominate. INEOS, leveraging US ethane feedstock, could emerge as a low cost producer in Europe, while others may shutter more assets deemed uncompetitive.

A new reality for chemicals

Industry analysts warn that the post-war trading system is ‘coming to an end’, forcing producers to rethink fundamentals.

Speaking on the ICIS Think Tank podcast, Paul Hodges, chairman of New Normal Consulting, said he believes the sector must pivot decisively toward regionalized production and sovereign supply chains.

“Export-orientated businesses are not going to work in future. That’s just unfortunately a fact,” he said.

Hodges highlights two critical trends: the need for local supply resilience and the resurgence of defence-related demand. “Defence is a massive opportunity for the chemical industry because you can’t have armaments without chemicals,” he noted.

With geopolitical tensions rising and NATO’s cohesion under strain, governments are racing to secure domestic production of critical materials, including ammunition.

Beyond defence, recycling and circular economy technologies will become increasingly important as producers seek to minimize reliance on imported feedstocks.

Hodges argues that realism must replace wishful thinking: “We can’t be guaranteed of export markets anymore because we’re moving into a protectionist world.”

For chemical producers, the next decade will demand agility, innovation, and a willingness to rethink the fundamentals of their business models.

Will Beacham is Deputy Editor at ICIS Chemical Business.