Engineer News Network The ultimate online news and information resource for today’s engineer

Engineer News Network The ultimate online news and information resource for today’s engineer

Electric vehicles (EV) face a critical challenge as the low-carbon transition hinges on sufficient battery production. Potential raw material shortages loom large, threatening to disrupt the demand-supply balance. The success of this green transition necessitates addressing these supply chain concerns to ensure a seamless and sustainable future for EVs and the broader low-carbon agenda, says GlobalData, the data and analytics company

GlobalData’s latest thematic report, Batteries – Thematic Intelligence, identifies the six sections of the batteries value chain. Of these, the raw materials, which are imperative to the development of batteries for EVs, will be a crucial factor as governments worldwide get serious about decarbonising their economies.

Thomas Pothalingam, Thematic Intelligence Analyst at GlobalData, comments: “The lack of low-cost, easy-to-purify raw materials to feed the world’s existing and planned battery gigafactories is the biggest threat to supply security. Demand for cheap, safe, high-performance, long-lasting, and low-carbon-footprint batteries will soar in the next 10 years—most notably from the automotive industry.

“Both the battery and EV industries will have to work closely with the public sector, capital markets, and other stakeholders to scale cheaper, longer-life, cleaner, and more recyclable batteries, battery components, and battery materials. New factories will be required.”

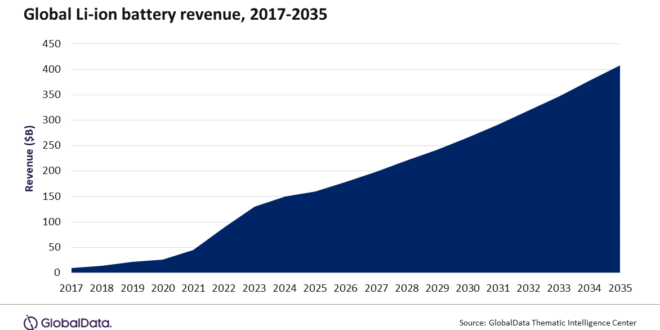

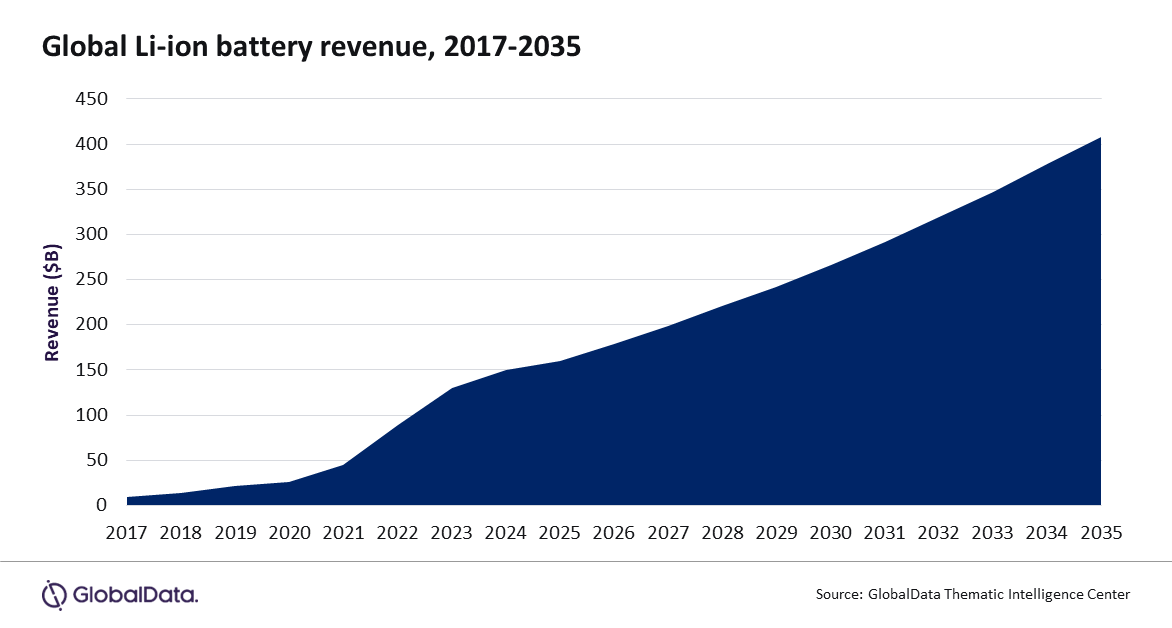

GlobalData forecasts the Li-ion battery industry revenues to increase at a compound annual growth rate of 12.5% from $88.6 billion in 2022 to $408.3 billion in 2035. Revenues from sales of Li-ion batteries for mobility end uses will drive much of the expansion, alongside considerable YoY growth in consumer electronics and energy storage.

As EVs increasingly shape the battery industry, automakers crucially consider consumer usage patterns when selecting battery chemistries. Addressing concerns about EV range remains pivotal, representing a significant barrier to widespread adoption and emphasising the importance of aligning technology investments with consumer needs.

Pothalingam continues: “The global transition to EVs will need an accompanying battery gigafactory expansion, which must be located near vehicle assembly plants. The rush to establish the necessary battery gigafactories to support the EV revolution brings value sources of FDI. The existing factory capacity cannot meet future demand, so massive capital expenditure must be invested into new gigafactories.”

GlobalData predicts CATL, BYD, LG Energy Solution, Panasonic, Samsung SDI, and SK Innovation to dominate the market in the mid-term. They control nearly 90% of global production and are forming close ties with the top dozen or so auto companies that are becoming progressively more vertically integrated structurally.

The industry’s consolidation also limits the potential of startups to technological innovation rather than gradually increasing battery production until they can compete with the six largest battery makers.

Pothalingam concludes: “Arguably, the single most important industry trend will be creating a massively scaled-up battery and battery materials recycling industry yielding a markedly circular battery industry by 2030. It will radically reduce the dependence on mined materials and the ecologically dirty mining industry. The US, Europe, and China are all embarked on developing their own local recycling industries, with Norway in the vanguard.

“Employing recycled materials reduces the dependency on issues such as mining output, ore grade, regional export quotas, geographic and political monopolies, and other unpredictable factors that make the market volatile. Recycled minerals also help reduce the environmental impact of mining and product development, an important factor to consider regarding emissions disclosure rules and access to green finance.”